We are very close now. I have spent most of the day for several days now working on long-term financing for the house.

We have paid for most of this in cash from the insurance money intended to rebuild a house for us in Pocatello. Following the horrible tornado season in 2011, most insurance companies changed their policies to allow people to rebuild on the site of their original house or to take their money and do anything they wanted with it. Our adjuster, seeing that we were near retirement age, told us about a couple who retired to the Southwest making it possible by building a smaller house and using he balance of the funds for part of their retirement investments.

Typically you receive 75% of the estimated replacement cost for your house. You start building and if things cost more than 75% you submit documentation for the difference and are given that amount of money. With our company, because they already gave you 75%, if you could rebuild your house for 60% you could keep the difference. If you chose to take the money and not rebuild your house, you only have 75% of the replacement cost.

That is what happened to us when we made this move to Montana. We though we could pay cash for a house and then have no mortgage making our retirement expenses lower. As we shopped, with the largest piece of money we had ever seen personally, clasped firmly in our hands, we thought we were rich. Very soon we realized that we were rich but that would not buy a house we could afford to have in any of the places we wanted to live.

After all the tumult of that past year, we decided to either find a perfect house and pay cash or take a little of the money and find or build a tiny place we could live in while we regrouped. Both were failures. A tiny house, such as a small kit house, on the cheap end, runs about $100,000 finished, plus whatever it takes for the land.

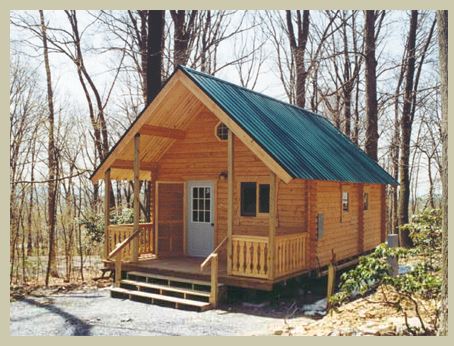

This cabin was one of our top picks. It cost $22,000 for the kit. After a foundaiton and kitchen etc, you could eek in at $75,000 or be luxurous at $125,000 but $100,000 seemed to us a realistic budget target. If you add land that is not in town, which we wanted, you must clear the land and have a driveway and usually a septic tank and well. Those could easily exceed the cost of the house. We abandoned the idea since we did not want to put all of our cash into a 700 square foot house with a 10″ x 8″ bedroom.

We considered looking for towns with very low cost real estate and then looking at really fix-er-uppers and at reducing our expectations. We made an offer on one house that was more than our cash and had a roof leak that traveled from the roof all the way down to the ground passing through the kitchen on its way to the downstairs. The owner would not come off his price and the cost was more than the value if we put the repair and the purchase together.

We decided we needed to go as far as we could in the best place we could find. As I have written here before we allocated our personal possession money to the house too. We had a lot of stuff already. We have clothes and a fully replaced kitchen. We have camping gear and rugs. We have some furniture. We can do more then more than fine with what we have. Others might consider it less than what they want but we want our house.

The house wear are building was going to be “lightly built” and we were going to finish it. Along the way it was coming together so beautifully we decided to continue to invest in it rather than stop when it was finished outside and about 60% finished inside. We have done a lot of the work ourselves and still we are going to have to take a mortgage.

One of the problems we are working with is that the real estate costs in Pocatello, ID were about 85% of the national average and we are now living where the costs are above the national average. Add that to having 75% of the replacement costs of the house and it is easy to see the parameters. Add to that we have a hand-crafted house and the mortgage is inevitable.

So here we are, almost at the finish line, looking for a way to finance the house. We are an excellent risk for the small mortgage we want. Most good mortgage risks put down 20% and take a mortgage for 80%. We are looking for putting down 80% and taking a mortgage for 20%. Our credit is excellent. We can document our retirement income. We have absolutely no other thing we are purchasing on credit. We do not even have a car payment. We have always been like that.

Others, including my mother, have told us to “live a little.” In the past 5 years we have taken some really exciting trips but still drive 10 year old, well maintained, cars that we own outright. All of this adding to the fact that we should be a no-brainer risk for a small mortgage.

But no. The most disconcerting aspect of this is that we have paid cash for the house so far. We want a mortgage that will cover the costs from April 1 to finish and pick up what we spent in March. We want the dreaded, “Cash back.” If we are classified as a refinance that is fine. We can do the cash back. But, the house is not a fully finished house so we don’t qulify for a refinance on a house that does not technically exist. If we do a mortgage on a new house we cannot get the cash back.

We tried to start out with cash then found that we should have opened a construction loan, taken nothing from it, and then built the house with cash up to the point we wanted a mortgage, use the construction loan after that and then roll that into a mortgage.

We have had a plan like that in the works for weeks. We filed all of the final paperwork 5 weeks ago and things are still not clear there. Because we were so close and it was not clear where we were going, I talked with some of the online mortgage people. They have been very nice and we have made the first steps with a couple of them but we are now caught in the situation of needing an appraisal on the house before we can find out if we qualify and the appraisals are $700. We must have one appraisal for each loan application.

So, here we sit. Are we a new mortgage and if yes, how do we get back the cash we used that we want to replace? Are we a construction loan with an end loan when we are sitting here at the almost complete place? Are we a refinance when we are not yet a house?

We don’t know. The completion date is one of the confusing elements of the equation. If we are completed, we are completed we are construction if we are completed we are construction. All of it hangs on the weather. The mill has to be able to get up the road to deliver our log siding and it has to be warm enough for the workers to be able to cut and lift the heavy logs.

Yesterday as our contractor and I mulled over the problem, I said, “What else is there to do other than the final installation of the plumbing fixtures and this little bit of trim?” He replied, “Get the kitchen counters in and pull the paper up and this will look like a new house.” If only we could find the right side of that gesture of pulling the papers up we would know what type of loan we needed.